Breaking down the numbers in 2023, looking forward to 2024, and the Govt.'s policies and their effects.

Too long; didn't read? Here's this week's TLDRs...

2023 – a year in review

2023 had two distinct halves, with a challenging first half and a later turnaround.

In April, sale volumes hit a 40-year low at 60,475, and national property values declined by 5%.

Turnaround signs emerged around May or June due to changes in credit cost and mortgage availability.

Mortgage rates increased but at a slower pace in 2023, with easing CCCFA rules from May 1st and relaxed LVR rules from June 1st.

Sale volumes increased in the second half, but listing flows remained relatively low.

Net inwards migration surged, affecting rental supply and accelerating rent prices in some areas.

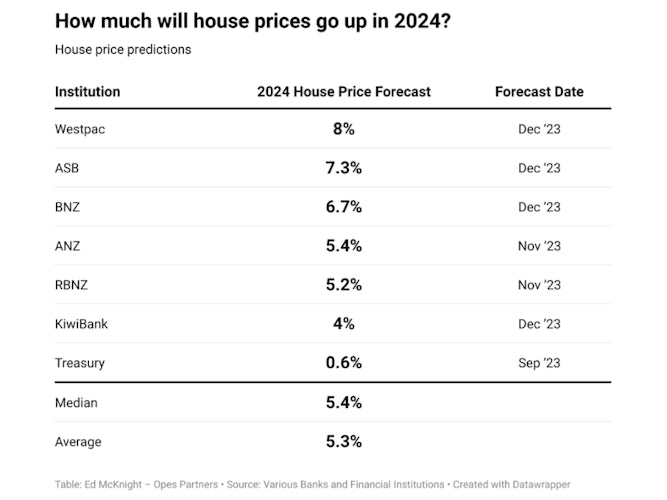

As the housing market enters the next phase in 2024, a property-friendly government aims to make changes to the Brightline Test and mortgage interest deductibility.

Anticipate a more subdued upturn in 2024, with a projected 10% increase in sales and 5% growth in prices.

Caps on debt-to-income ratios are expected in 2024, and high mortgage rates currently restrict risky lending.

Read the article

Read the article

The stats from Core Logic

Highest median value: Herne Bay (Auckland) $3,161,400

Lowest median value: Cobden (Grey) $258,200

Highest 12-month change in median value: Sunshine Bay (Queenstown) 6.6%

Lowest 12-month change in median value: Featherston -16.0%

Highest five-year change in median value: Mataura (Gore) 138.9%

Lowest five-year change in median value: Auckland Central -8.8%

Top sale price: 120 Victoria Avenue, Remuera, Auckland (18 Jul) $23,800,000

Highest change in median rent: Fairview Heights (Auckland) 32.4%

Lowest change in median rent: Herne Bay (Auckland) -14.5%

Highest gross rental yield: Whanganui (suburb) 8.5%

Lowest gross rental yield: Whitford (Auckland) 1.1%

Shortest days on market: Hargest (Invercargill) 11 days

Longest days on market: Ohakune (Ruapehu) 115 days

Read the article

Read the article

An interesting read written by Kiwibank’s chief economist Jarrod Kerr this week: the talking-points of the state of the Kiwi housing market.

Everything that is wrong with our housing market is due to a lack of supply. But policymakers focus on demand. We need better infrastructure, more plots, more houses. And affordability will follow.

Kerr notes three spikes in population growth, noting the correlation between migration and rising property demand and prices.

We’ve seen a lack of increased spending on infrastructure despite significant migration-driven housing shortages.

There’s a need for an increased supply of land and utilities for development to address population surges.

Kerr suggests solutions like self-funding infrastructure funds and scaled-up builders, requiring political will and execution.

Despite an increase in tradie migrants, a fall in consents and soft pre-sales indicate a decline in housing activity and prices.

Kerr anticipates a role for migration and government policies in worsening the demand/supply imbalance in the housing market.

He predicts interest rates may fall in 2024, but the Reserve Bank's threat to hike again poses a risk.

Kiwibank economists estimate a 5-to-7% rise in house prices in the coming year, with demand likely to outstrip supply.

Kerr points out the need for approximately 50,000 to 60,000 new dwellings for every 120,000 people, highlighting the supply-demand imbalance.

He expects the residential construction boom to cool, with supply falling into the low-to-mid 30,000s, posing challenges unless significant policy changes occur.

Read the article

Read the article

How house prices have changed, here and abroad.

Lower global interest rates post-COVID fuelled a worldwide surge in house prices as buyers borrowed more at cheap rates.

New Zealand stands out for its rapid pre-COVID house price increase and subsequent sharp decline, unlike other countries.

After 12 interest rate hikes, New Zealand's house prices fell by 14%, with Auckland and Wellington seeing up to a 20% decline.

Despite the fall, New Zealand's average house price remains about 25% above pre-COVID levels.

Factors influencing house prices in other countries include long-term fixed mortgages in the US, migration-driven demand in Australia, and longer-term fixed terms in Canada.

The UK experienced a steady increase in house prices, up 25% since COVID, attributed to low unemployment, construction cost inflation, and pent-up demand.

Despite varying global interest rates, house prices in many countries increased due to low supply, inflation, rising incomes, and low unemployment.

The USA, with over 40% house price increase, stands out due to a lack of supply caused by homeowners with low fixed-rate mortgages.

Read the article

Read the article

Subdued uptick in the market through November

November showed an increase in housing market activity with sales up 12.2% from the previous year.

However, November sales were the lowest for the month since 2011, except for the previous year.

Sales were below down 37% from the peak in November 2020.

Prices slightly increased, with the median selling price up 0.1% for the month.

The House Price Index (HPI) increased nationally by 0.8% for the month and 2.7% over the last three months.

Price trends around the regions were mixed, with five regions showing an increase in HPI compared to October, and seven recording a decline.

Read the article

Read the article

An investor’s analysis of regional house price movement - Ed McKnight

Housing market recovery signs are evident, with steady price growth since June reported by the Real Estate Institute of New Zealand and OneRoof.

A common belief is that property prices rise faster in bigger cities, but data analysis challenges this assumption.

Since 1992, Gisborne, the smallest region, experienced an average annual property price increase of 6.4%, surpassing larger regions like Wellington (6.2%) and Canterbury (5.9%).

While Auckland had the fastest property price increase, larger populations in big cities don't necessarily correlate with faster price growth.

Bigger cities have both higher demand and greater supply, levelling out the rate of price increase in the long term.

Property prices in bigger centres tend to increase more consistently than in smaller towns, which may have more fluctuations.

Consistency is essential for property investors, as growing house prices contribute to wealth accumulation and psychological motivation to stay in the market.

Investors in larger cities may grow their portfolios faster due to more consistent and predictable price increases.

Read the article

Read the article

How will the new govt. tackle the housing supply issue?

The New government plans significant changes to housing supply policies, including:

Repealing the Natural and Built Environment Act (NBEA) and the Spatial Planning Act, replacing them with amended Resource Management Act (RMA) to ease infrastructure consent.

Making Medium Density Residential Standards (MDRS) optional for councils, abandoning a bipartisan housing intensification deal, impacting short to medium-term house prices.

Considering sharing a portion of GST from new residential builds with councils.

Exploring the option for home builders to opt out of building consent with long-term insurance.

Requiring councils to zone land for 30 years of housing demand immediately to address land availability.

Introducing a $1 billion Build-for-Growth fund, rewarding councils with $25,000 for every house delivered above the five-year average.

Planning to reform the Infrastructure Funding and Financing Act to reduce red tape and prioritise housing growth in transport funding.

Amending the Building Act and Resource Consent system to allow easier development of small structures like granny flats.

Read the article

Read the article

TA: A look forward to 2024

Statistics NZ data indicates a net gain of 129,000 people in New Zealand, boosting the population by 2.5%.

Demand for accommodation is rising, while the supply of new dwellings is falling, with consents down 21% over the past year. This imbalance will drive higher rental prices.

As interest rates fall, property purchases may become more affordable, further increasing demand and putting upward pressure on prices.

The return of interest expense deductibility for investors is already leading to increased demand.

These factors are anticipated to outweigh the impact of rising unemployment, resulting in a more significant average increase in house prices than seen in 2023.

Read the article

Read the article

OCR rates cuts should dominate next year

New Zealand's GDP for the September quarter contracted by -0.3%, leading to concerns about the timing of OCR cuts.

The technical recession over the last summer, initially revised away, has been revised back in, indicating a weaker economy than previously thought.

Economic activity per person contracted by 0.9% in Q3, with the economy down over 3% for the year.

Kiwibank's economists anticipate another contraction in the fourth quarter and possibly the first quarter of the next year, suggesting a potential double-dip recession.

The RBNZ's restrictive monetary policy is seen as contributing to the economic challenges, and rate cuts are being discussed as a response.

Financial markets have reacted with a drop in rates and a slight decrease in the currency value, with discussions of potential OCR rate cuts dominating.

The US Federal Reserve's "dovish" stance and indications of rate cuts have influenced market expectations.

Kiwibank suggests the RBNZ may start cutting rates in November next year, a year ahead of its projections, anticipating a shift from the current rate hike risks.

Read the article

Read the article

DTIs still a possibility

Finance Minister Nicola Willis is awaiting advice from the RBNZ before deciding on the implementation of DTI restrictions.

While implementing DTIs doesn't require government approval, RBNZ has historically consulted with the Finance Minister before introducing new tools.

A recent RBNZ article suggests that if DTIs had been introduced before COVID-19, fewer borrowers would be struggling with higher interest rates.

Banks have been informed to be ready for DTIs from April 2024 if implemented.

A Bank of International Settlements case study claims that DTIs are effective in supporting financial stability and sustainable house prices, with a smaller impact on first-time buyers than investors.

The study indicates that LTV restrictions have contributed to household and lender resilience, but their impact on house price inflation is limited and temporary.

LTV restrictions may have unintended consequences, including restricting lending to creditworthy borrowers and impacting housing supply.

Read the article

Read the article

NZ’s new tax reforms are undoing the mistakes of the past

The new coalition government in New Zealand announced tax reforms, allowing property investors to deduct interest costs retroactively from April 1, 2023. The changes overturn the previous Labour government policy that phased out interest deductions for landlords, which was punitive and didn’t provide clear housing affordability benefits. The National Party plans to reduce the brightline test period from ten to two years. While criticisms of the new policy are valid, it aims to rectify a flawed law, removing the denial of interest deductibility introduced in 2021. Inland Revenue had warned against the 2021 change, citing potential rent increases and adverse effects on housing supply, stating it eroded tax system coherence. The removal of interest deductibility departs from the fundamental tax law principle of offsetting costs associated with producing taxable income.

Read the article

Read the article

Development group fined $133,000

Development group The Guardian group and its contractors were fined $133,000 for building without consent in Auckland.

The group knowingly constructed five pavilions for restaurants and retail without building consent.

Text messages revealed a defiant attitude, expressing intentions to proceed despite compliance issues.

Auckland District Court ruled in favour of the council, imposing fines totaling $133,000.

Read the article

Read the article

Landlord to pay $4,000 for emotional damages to ‘boarder type’ tenant.

A North Shore landlord must pay a tenant $4,000 for emotional harm after a dispute over a damaged bedroom door led to strained relations. The tenant repaired the damage without notifying the landlord, resulting in a heated argument. The tenant later gave notice, and various issues, including power and water disruptions, ensued. The tribunal dismissed the landlord's general damages claim and awarded $2,672 to the landlord for other claims. The landlord claimed a "boarding type" situation, asserting the Residential Tenancies Act didn't apply, but the tribunal disagreed. The tenant received $4,000 for emotional harm, and the landlord faced fines for breaches, emphasising the importance of landlords accepting responsibilities under the RTA.

Read the article

Read the article

Aus to 3x fees on foreign purchasers

Australia plans to triple fees for foreign buyers purchasing existing homes to increase the supply of affordable housing.

The move is part of broader measures, including higher penalties for vacant properties and enhanced compliance activities.

The Labour government aims to align foreign investment with the goal of boosting the nation's affordable housing supply.

Application fees for foreign investment in "build to rent" projects will be reduced to encourage more home construction.

The fee adjustments follow last year's decision to double fees for foreign investors, expected to generate A$455 million in additional revenue over four years.

The government intends to implement the higher fees through legislation in 2024.

Australia's housing market faces steady growth in prices due to rising demand surpassing supply in the nation of 26 million people.

In June, the government pledged A$2 billion to create thousands of new affordable homes nationwide, focusing on increasing public housing for those on waiting lists.

Read the article

Read the article